This survey aims to understand the state of non-financial support in Latin America and the Caribbean. For this study, Latimpacto and Red de Impacto conducted two separate surveys in 2021: one survey was completed by non-financial support providers, while social purpose organizations responded to the other. This allowed us to identify gaps, trends, and opportunities between providers and recipients.

Who uses and provides non-financial support?

The sample of providers showed that most (40%) are non-governmental organizations and foundations. The rest are business support organizations (15%), impact funds (9%), consulting firms (9%), corporations (7%), universities and think tanks (3%), family offices (2%), and others (16%) (see graph 1).

Source: Prepared by the authors based on survey results.

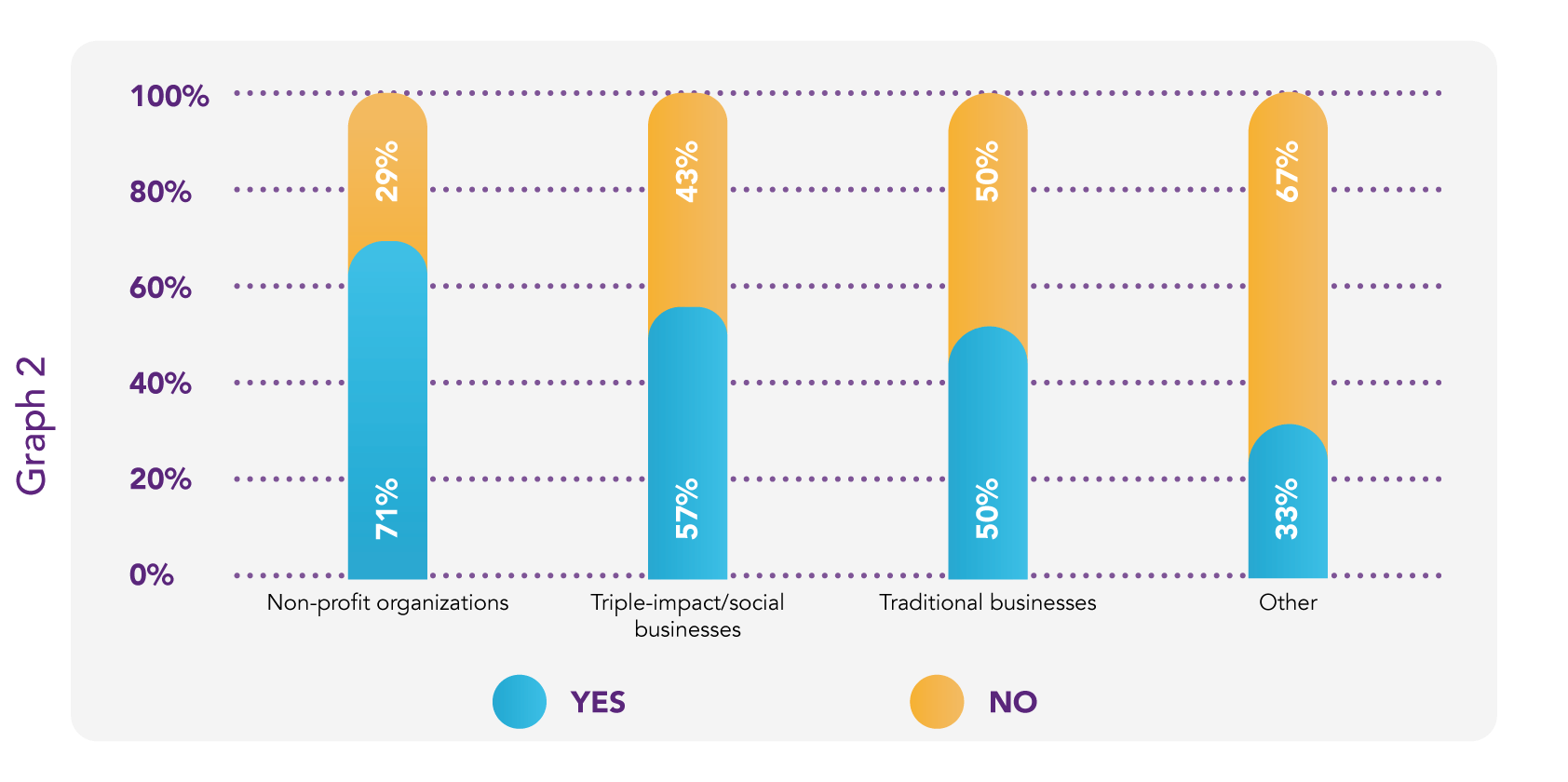

As for the demand for non-financial support, the survey showed that non-profit organizations are the primary recipients (71%), followed by triple-impact/social businesses (57%) (see graph 2).

Source: Prepared by the authors based on survey results.

Additionally, most surveyed organizations (58%) reported that they receive any type of non-financial support, with a large proportion (43%) receiving it from business support organizations. Thirty-eight percent of surveyed SPOs are in the consolidation stage, that is to say, having operated for five years or more (see graph 3).

Source: Prepared by the authors based on survey results.

What are the gaps between the services that are considered necessary and those that are offered?

We compared the supply of non-financial support services available to those considered essential by providers. Services such as impact management measurement and strategy seem to be meeting needs on perception of their importance (see graph). Nonetheless, a gap of services was observed for soft skills and financial sustainability.

Source: Prepared by the authors based on survey results.

What type of non-financial support is offered based on the financial instrument provided?

The survey results show that, in absolute terms, 32% of respondents offering non-financial support do not provide any type of funding. In contrast, 68% percent provide non-financial support along with one or more financial instruments. Among respondents providing a financial instrument, we can identify donations (20%), followed by hybrid finance (18%), equity (16%), and debt (14%). In relative terms, equity is the financial instrument that provides the most non-financial support (94%), followed by donations (90%), debt (87%), and hybrid finance (85%) (see graph 5).

Source: Prepared by the authors based on survey results.

Source: Prepared by the authors based on survey results.

As described earlier, among the services perceived as more necessary by non-financial support providers are strategy, soft and technical skills, and financial sustainability[1]. However, prioritized services vary considerably depending on the type of financing offered (see figure 4).

[1] The other services with less priority are, from high to low, impact management and measurement, access to markets, ecosystem development and access, and managerial and administrative skills.

We also surveyed social purpose organizations to learn about their non-financial support experience. The three most common services received were strategy, managerial and administrative skills, and soft skills. Nevertheless, these vary depending on the SPOs’ development stage and years of operation (see figure 5). A transition can be observed from early-stage organizations’ soft skills to strategic strengthening support for more matured organizations.

Source: Prepared by the authors based on survey results.

What proportion of the non-financial support providers evaluates the impact of the support offered?

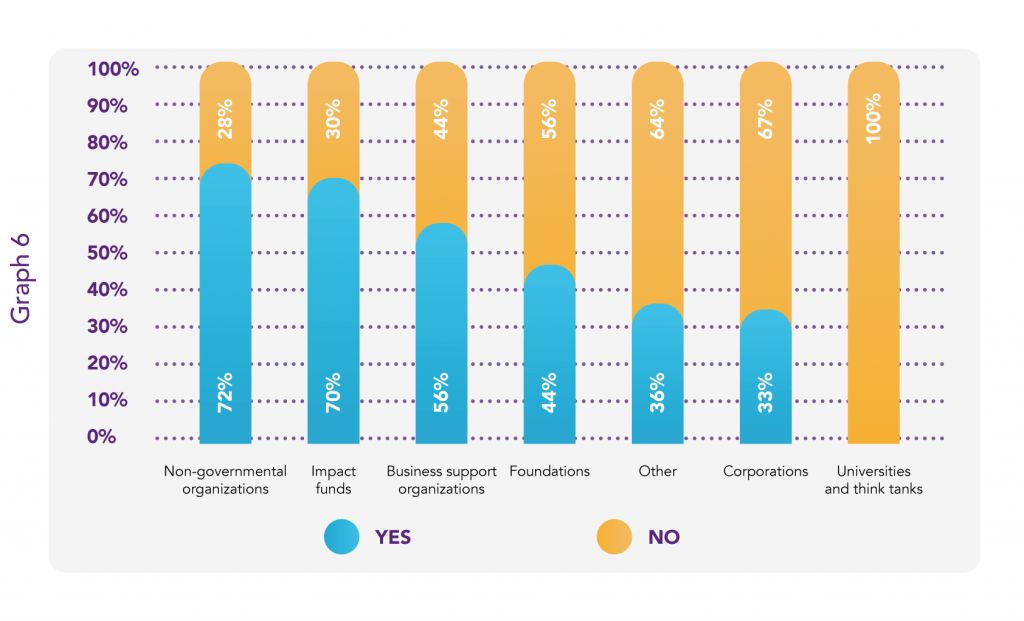

Half of the non-financial support providers responded that they evaluate the impact of the support they offer. Within this group, non-governmental organizations and impact funds are the ones that do it the most (see graph 6). The core evaluation topics are social and environmental impact, followed by an increase in sales or profitability, increased organizational capacity, satisfaction with the service provided, and learning systematization.

Source: Prepared by the authors based on survey results.

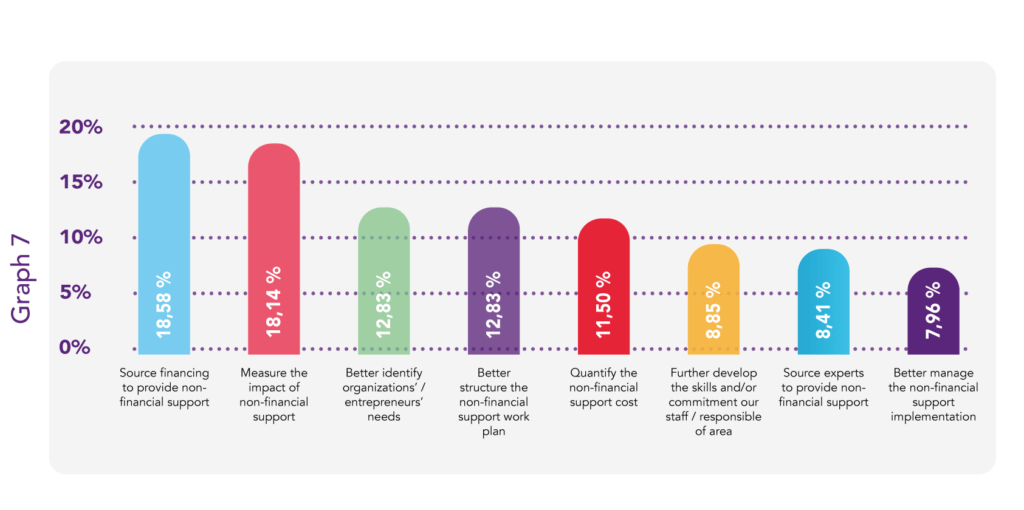

Which practices offer more room for improvement?

Graph 7 shows practices that non-financial support providers identified as improvement opportunities in their organization—obtaining funds to provide the non-financial support and measuring the impact of non-financial support as the two most common responses.

.

Source: Prepared by the authors based on survey results.

How is non-financial support offered, and how long does it last?

Fifty-nine percent of non-financial support providers in the sample offer it directly (for example, through their staff or by participating members of their boards of directors), while the rest (41%) do it indirectly (for example, through consultancy or partners and networks). Consultancy, courses, and/or group workshopsand services through partners and/or networks are the most common forms of delivery (see graph 8).

Source: Prepared by the authors based on survey results.

Additionally, most non-financial support initiatives last for one year or less, varying between 6 and 12 months (39%) and 1 and 6 months (26%) (see graph 9).

Source: Prepared by the authors based on survey results.

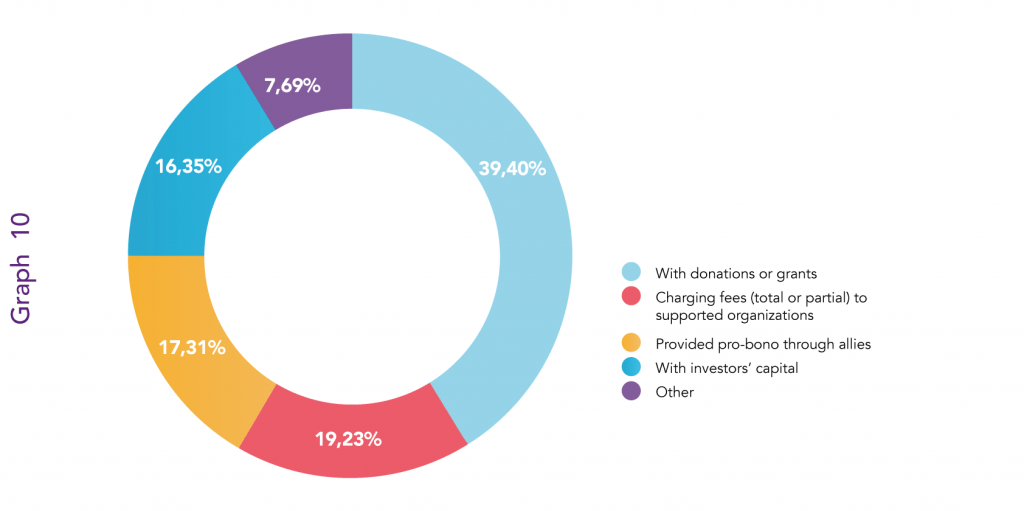

How is non-financial support financed?

Among the reported sources of funding for non-financial support, the main ones were donations or grants (39%), followed by total or partial payment for the services received by the SPOs (19%), pro bono services by allies (17%), investor capital (16%), and other sources (graph 10) [1].

[1] Other reported funding sources for non-financial support were collaborations, interests earned annually from the initial capital offered, international cooperation projects or tenders, among others.

Source: Prepared by the authors based on survey results.